Come on, admit it. Don’t you feel just a little satisfaction watching 37 million adulterers exposed in the Ashley Madison hack? “They do kind of deserve to be cheated just a bit for being cheaters,” someone in one of my keynote speeches commented.

In this case, the hackers weren’t seeking money, they were seeking revenge. Their goal was to get Ashley Madison to shut down the site because they said it wasn’t living up to it’s own privacy policy (they weren’t). But to side with the hackers is a bit like saying it’s okay to pepper spray customers to keep them from going into a store you’re morally opposed to. In other words, be careful when you condone the use of customers as pawns to fuel change. You just might be the next customer to become a victim, and your data could be just as sensitive (your medical records, divorce proceedings, kids’ geographical location or your online video viewing habits).

I’ve had dozens of media requests for interviews and countless more email inquiries from people concerned about the Target data breach. At first, everyone just wanted to know details of how it happened, how big the breach was, and what they should do about it if their credit cards were at risk. Now that the initial shock of it is over, we are on to a bigger question:

How do we keep breach from negatively affecting so many Americans?

Breach will always happen. If it’s digital, it’s hackable. It’s coming to light that the Target breach may have been due to the computer access an HVAC WORKER (no, not an entire company, an individual WORKER) had to Target’s systems. While there is no guaranteed way of preventing fraud, there is a pretty reliable answer out there, and it’s been around for decades. That answer is for the US to finally catch up to more than 80 countries around the world and start using chip and PIN enabled credit cards, also known as EMV, smart cards, or microchip cards.

When the finance chief of a London hedge fund got an urgent phone call about possible fraud on a Friday afternoon just as he was preparing to leave work, he honestly thought he was doing the right thing by giving the caller the information requested. Wouldn’t any decent CFO want to stop fraud if it was in his power to do so? That way, he could rest easy for the weekend, knowing he had saved the company from damage. Imagine the feeling in the pit of his stomach when he turned on his computer Monday morning to find that 742,668 pounds ($1.2 million) was missing!

That’s what happened to Thomas Meston of Fortelus Capital Management LLP in December of 2013. He received a phone call from someone claiming to be from Coutts, the London-based hedge fund’s bank, and the caller warned him there may have been fraudulent activity on the account. Meston was reluctant, but agreed to use the bank’s smart card security system to generate codes for the caller to cancel 15 suspicious payments.

Over the next ten years, wearable technology could change the way you live even more than smartphones have. Wearable technology combines all of the tracking, collecting and communicating power of current mobile devices with an intimate level of personal information captured in real-time. Common wearables include: Fitness Bands, GPS-enabled Cameras, Digital Glasses, Medical Devices and Smart Watches. Wearable technology can be a force for good, but you need to consider the privacy and security implications of the devices as well.

For the moment, wearable technology is more like a trendy hobby for early adopters than it is a means of recording highly accurate & useful information. In the future, businesses will likely utilize wearables to monitor everything from hours spent working to employee whereabouts throughout the day. It is this enterprise usage that will ultimately fuel the adoption of wearable technology in the consumer market. For now, your smart watch is a fun and shiny object with a few killer apps much like the computer back when email was introduced. Ten years from now, you might wonder how you lived without the increased convenience and connectivity.

You’ve made it home safely after braving gastronomic adventures at greasy spoons, drinking from questionable water sources, and surviving white-knuckled taxi rides. Now, post those vacation pictures on social media and wrap up the loose ends of protecting your identity.

Monitor Your Accounts: Shortly after you return from your travels, pay special attention to your account statements to make sure that nothing out of the ordinary appears. If a credit card number or bank account number was stolen during your trip, this is how you will catch it early and keep it from becoming a major nightmare. Contact your provider and alert them to the breach immediately.

Get a credit report: Hopefully you’ve monitored your accounts throughout the trip. When you get home, request a report at www.annualcreditreport.com. Check your credit report for any suspicious activity. Even if you don’t see any unfamiliar transactions, that still doesn’t mean you’re safe.Identity thieves are known to take their time and act when you least expect it, so continue monitoring!

Welcome to the third (and longest!) part of our four-part series on travel safety. We’ve covered “Planning Your Trip” and what to do “Before You Go” Today we’ll go through the many important things to consider while you’re “On the Road”. Be sure to check back tomorrow for our final installment of what to do “When You Return”.

1. Travel Light:

If you don’t have to take it with you, increase your safety and leave it at home. This includes:

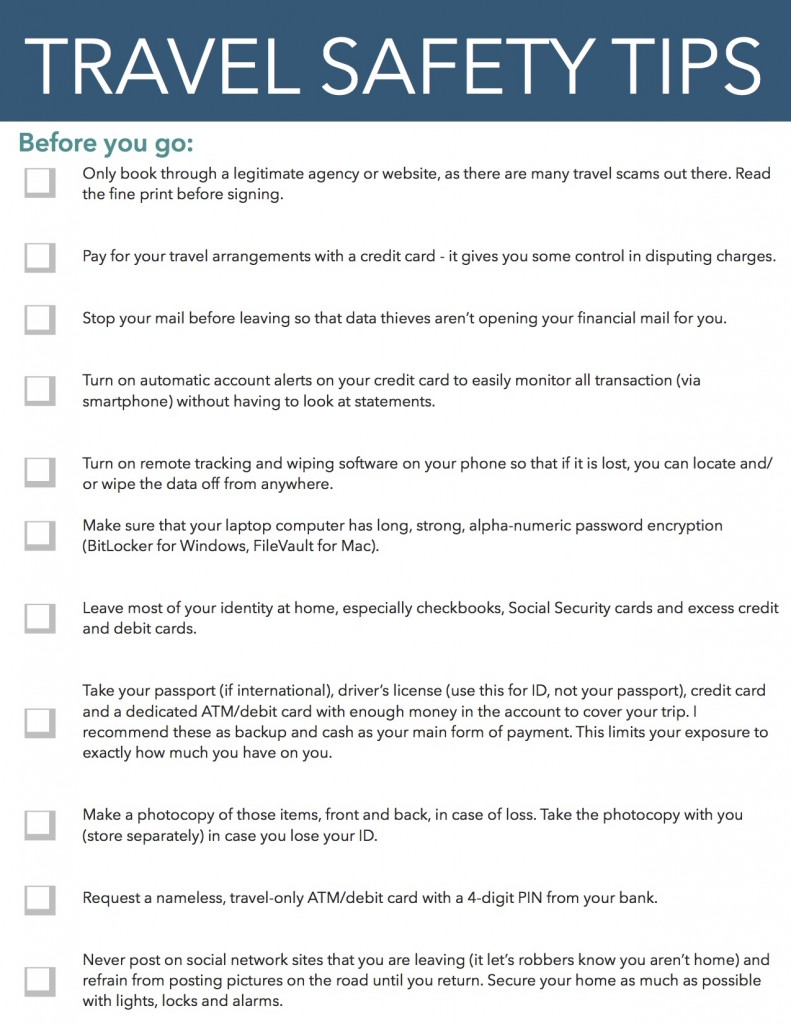

Checkbooks: Do not carry checks or take only one or two for an emergency, placing them with your cash in your money belt. Checking account takeover is one of the simplest crimes to commit and one of the most devastating types of financial fraud from which to recover. The easy alternative? Use a credit card or cash.

This is part two of our four-part series on travel safety. Yesterday we covered “Planning Your Trip” and in the next few days we’ll discuss “On the Road” and “When You Return”. For today, we’ll look at steps to take after your trip is planned, but before you go.

Photocopy the contents of your wallet/documents: Or make a list of all the contents and all your travel documents to carry with you in a protected place as you travel. It’s also a good idea to leave a copy at home with a trustworthy person whom you can contact. It will save you hours of frustration if anything is lost or stolen.

Protect your accounts: Place a travel alert on your credit card accounts so the bank will know why charges from some lovely resort are suddenly showing up. You can also freeze your credit so no new accounts can be opened while you are away. Finally, turn on automatic account alerts on your credit card to easily monitor all transaction (via smartphone) without having to look at statements.

Today I begin a four-part series on travel safety to protect your identity before during and after your trip. I’ve tried to make this series comprehensive for all stages of travel. Today we’ll cover Planning Your Trip , to be followed in days to come by: Before You Go, On the Road and When You Return.

While you may be aware of the basics, the lists in these blogs show you how to think like the criminals think. Be proactive and outwit them at their own game!

Use a legitimate agency: Verify the business you are booking your trip through. If you are going to use a travel agency or online booking company, make sure they are authentic first. Go online and do your research – if people have been swindled before by the company, the Internet is the first place they will go to vent. You can even ask the company for references so you can check up on some satisfied customers. Also, investigate the travel companies with the Better Business Bureau (www.bbb.org) and the attorney general’s office in the state where the company does business. (www.naag.org).

Get monthly strategies and tips for protecting yourself and your business delivered right to your Inbox. Signup now and you'll immediately receive John's 7 Survival Strategies for Starving Data Spies!