Reading Credit Reports

A credit report is a history of how you or your company borrow and then pay off your credit, including delinquency and bankruptcy. There are currently three main credit bureaus in the United States—Equifax, Experian and TransUnion. If you own a home, have a credit card, lease a car, or apply for or use credit of any sort, this information is reported to one, two or all three of these credit bureaus. In addition, they collect information on how timely you pay your bills, how often you are tardy, how frequently your credit is checked by companies and any changes of address, employment, or personal information.

By monitoring these reports closely, you will know when someone else is using your credit rating to their benefit. If an identity thief opens a new credit card or takes out a loan using your Social Security number, you will see it on your report. The quicker you spot the problem, the less trouble it will cause. Monitoring your credit report is the single most effective monitoring tool available to keep minor identity theft from turning into full-scale identity fraud.

Ordering Your Credit Report

Order your credit report from the first of three agencies (listed below). By law, you are entitled to one free report from each agency once a year. The easiest way to get a report is to visit www.AnnualCreditReport.com or call 1-877-322-8228. Make sure that you request your free annual credit report from one credit agency only, as you will order the other two reports throughout the remainder of the year. By spreading the reports out over time, you will be monitoring your files consistently and frequently.

Be prepared to have your account information handy. Even when applying for your free credit report online, you will reach a screen that instructs you to call in to ‘Confirm your Identity’. The representative will ask you a series of questions that range from your current and past addresses, bank and credit card account numbers, the date the accounts were opened/closed, mother’s maiden name, and date of birth. They may also ask you the amounts that you have taken out in loans. Don’t get discouraged by the process. This is just another way they are protecting your identity by ensuring they give this information out to the right person. And since you have initiated the call, you are in control of the flow of information.

Skip ahead 4 months from today on your calendar, and mark down the following information:

Request & Review Next Credit Report—Return to www.AnnualCreditReport.com or call 1-877-322-8228. The second time you request your report, choose a credit agency that you didn’t chose the first time (e.g., if you chose Equifax first, choose Experian second, TransUnion third and back to Equifax one year from today).

Skip forward 8 and 12 months on your calendar and mark down which credit bureau you should request a credit report from. On month 12, you will be requesting the report from the same credit bureau that you requested it from the first time. If you use an electronic calendar, schedule this as a recurring event for every four months—that way you will be automatically reminded every time you should review your credit. While ordering your credit report may not be the easiest or most hassle-free process, it is the MOST effective way to monitor identity theft and worth your time.

Equifax

P.O. Box 105788

Atlanta, Georgia 30348

Toll Free: 1-800-685-1111

TransUnion

P.O. Box 6790

Fullerton, CA 92834

Toll Free: 1-800-888-4213

Experian

P.O. Box 9554

Allen, TX 75013

Toll Free:1-888-397-3742

Reading Credit Reports

When you receive your first credit report, follow these steps:

- Completely read through the entire report and the definitions that the credit reporting agency gives you so you understand how to interpret the information. While reviewing your report a second time, use a highlighter to mark any accounts that you don’t recognize or that appear to contain inaccurate information (e.g., negative credit feedback where there should be none), and a different colored highlighter for any accounts that you no longer need or use.

- Contact the credit bureau about any accounts that you have highlighted because you don’t recognize them or because of erroneous information. Be aware that some companies give you a credit card with their name on it (like Sears) that is issued by another company (GE Capital). You may need to do some research on your credit card statements to understand who actually issued the card. The credit bureau should help you work through the questionable information. To get through more quickly to a human being at the credit bureau, get in contact with the fraud department, which has more reason to take your call.

- Call and cancel all of the accounts on your credit report that you no longer need or use. Please be aware that canceling credit accounts can affect your credit score (sometimes it will lower the amount of credit you have available), so only do this in conjunction with your accountant or financial counselor. If done over time, and in the right way, it won’t adversely affect your credit score. Make sure that you call the company that issued the card or loan, not the credit bureau. For example, if you have five credit cards that you no longer need (and probably have forgotten you even had), call each credit card company, settle any balances and cancel the account. This is another means of Eliminating the Source. It minimizes the number of places that a thief can take advantage of your credit. If you do not wish to lose the credit value from those accounts, simply monitor them to make sure that no money is ever spent on them.

- The next time you review your report, you should look for any changes as compared to the previous report. If there are changes, make sure that it is credit that you applied for, and not a new account set up by an identity thief. You will probably have very little work to do on future versions of your credit report as most of the hard work is done on the first round. Use this first time to educate yourself about credit reports and to clean up the years of neglect and identity creep.

- Make sure to have your spouse or partner order and monitor their credit reports, as they are mostly independent of yours. If your children are older than 16, I recommend that they monitor their credit reports as well, with your help.

Understanding Credit Reports

Once you have obtained access to the report, look for accounts you don’t have, inquiries you didn’t make, credit cards you didn’t open, residences you never lived at, court actions in other states, or unexpected changes to your credit rating.

Sections of a credit report:

- Personal Information—A personal profile

- Names

- Residences (Current and Previous)

- Social Security Number

- Date of Birth

- Driver’s License Number

- Telephone Numbers

- Spouse’s Name

- Employer’s Name and Address

Any discrepancies with the information in your credit report could be a sign of fraud. You should file a dispute with the credit bureau for all your personal information discrepancies.

Credit Summary—History of all opened and closed accounts under your name:

- Source (i.e., Bank Name/Address)

- Date Opened/Reported Since

- Type/Terms/Monthly Payment

- Responsibility

- Credit Limit/Original Amount/High Balance

- Recent Balance/Recent Payment

- Status Details

Lenders are not required to send your information to all three bureaus, so loans are sometimes only reported to one bureau, which can create discrepancies between different credit reports. In addition, some reports provide a history of balances for each of the lenders while others do not. It is important to review all three credit reports throughout the year to see if any fraudulent accounts have been opened under your name. Any accounts you didn’t open or any loans that are not yours should be disputed.

- Public Records—Court actions coming from federal, state, and county court records:

- Bankruptcy

- Tax Liens

- Monetary Judgments

- Overdue Child Support Payments

If you find any discrepancies such as court actions from states you have not lived in, file a dispute with the bureau.

- Credit Inquiries—There are two types of inquiries, Hard and Soft:

- Hard Inquiries—You initiate the inquiry by filling out a credit application. These inquiries influence your credit rating and should be kept to a minimum.

- Soft Inquiries—These inquiries include pre-approved credit cards or pre-employment screenings and can only be seen by you. They do not affect your credit rating.

If you did not apply for a loan or credit card that appears in this section, file a dispute with the bureau.

- Credit Rating/Credit Score—Provides an indication to lenders of your credit risk:

- All three credit bureaus use their own rating system (Equifax— BEACON, Experian—Fair Isaac Risk Model, TransUnion— EMPIRICA)

- The higher your score, the better your credit rating

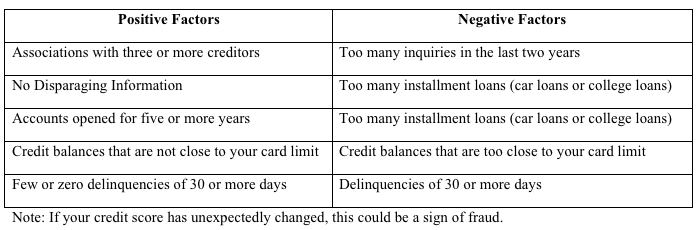

Your credit rating is affected positively and negatively by many factors, for example:

Remember, the quicker you spot the problem, the less trouble it will cause. Monitoring your credit report is the single most effective tool available to keep minor identity theft from turning into full-scale identity fraud. Freezing your credit is like locking your credit file with a password.

For a more convenient way to monitor your credit reports, along with other sources of identity risk, consider subscribing to one of the few reputable, useful identity monitoring services. To learn how to protect your identity, at home and in your business, read Privacy Means Profit.

Sorry, comments for this entry are closed at this time.

Connect with Sileo

The Sileo Report Newsletter Signup

Get monthly strategies and tips for protecting yourself and your business delivered right to your Inbox. Signup now and you'll immediately receive John's 7 Survival Strategies for Starving Data Spies!

Get monthly strategies and tips for protecting yourself and your business delivered right to your Inbox. Signup now and you'll immediately receive John's 7 Survival Strategies for Starving Data Spies!

No Comments Yet

You can be the first to comment!